")

")

We study the European

taxation needs of

global companies.

IVA CONSULTA

Glorieta de Quevedo, nº 9, 5º

28015 Madrid (España)

CENTER OF SERVICES

C/ Arena, 1, Planta 4ª

35002 Las Palmas de Gran Canaria (España)

Blog

Non-resident companies and Spanish e-regulations

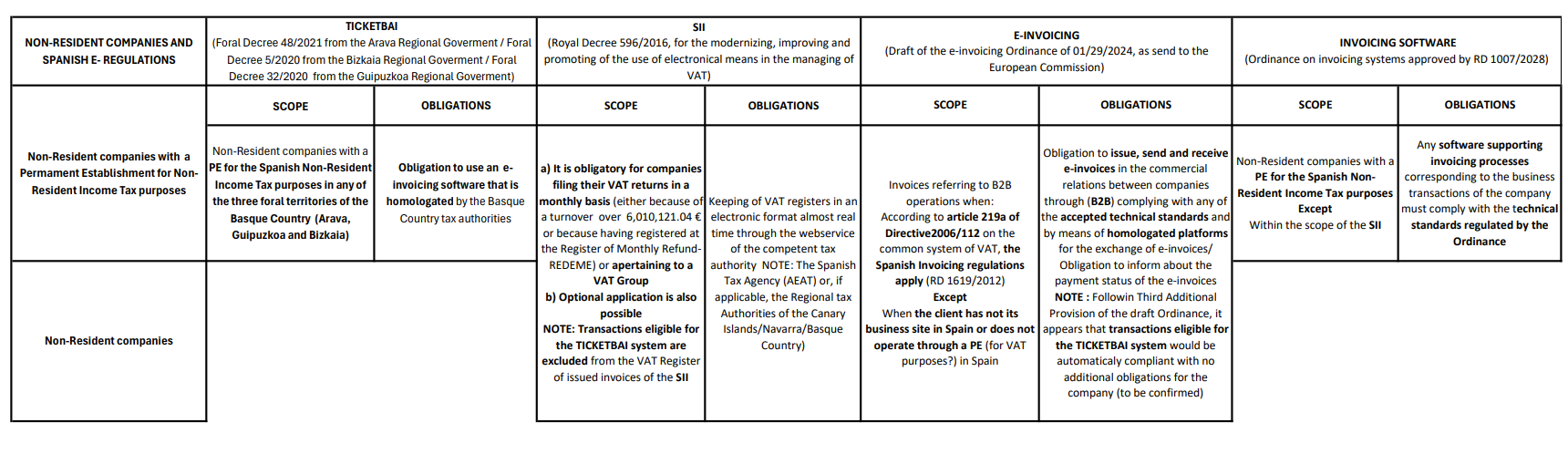

As the final stage before its approval, the Spanish Government has notified the European Commission the final draft of the Ordinance that regulates B2B e-invoicing obligation in Spain (Draft Royal Decree implementing Law 18/2022 of 28 September 2022 on the creation and growth of companies with regard to electronic invoicing between companies and professionals).

This regulation develops the extension to B2B transactions of the obligation to e-invoice introduced by Law 18/2022 of 28 September regulating the creation and growth of enterprises, that modified article 2bis of Law 56/2007 of 28 December of Measures to Promote de Information Society.

In practice, this obligation will not be effective until 12 (24 for companies with a turnover under 8 million Euros) months elapse since the e-invoicing Ordinance is published at the Official Gazette.

To be confirmed in a case by case basis, it is to be assume that non-resident companies operating in Spain which, regardless of being VAT taxable subjects, do not have a permanent establishment for Non-Resident Income Tax purposes, should be marginaly affected by the e-invoicing Ordinance. This is so due to the exclusion from the scope of the Ordinance of those B2B transactions where the destinee is not a tax resident nor operates through a permanent establishment in Spain.

However, it is to be remembered that e-invoicing is only one of the aspects related with tax technology which are regulated in Spain, so the need for any non-resident company operating in the Spanish market to closely analyze its position regarding the legal framework on this field.

With the aim of helping in this task, we attach a summary of different regulations affecting invoicing and data reporting in Spain and how they can affect non-resident companies:

Other entries on this topic:

E-invoicing in Spain. Present and future scenario for non-resident companies

Spain: Current status of mandatory e-invoicing on B2B operations

Spain. The new VAT e-commerce regulations and the SII obligations for non-resident companies

Stay Informed

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

About the author

Categories

Subscribe!

Tags

Travel VAT Conference 2022

VAT

step plan

fiscalidad

Reino Unido

digital AGE

non-reusable plastic plackings

sentencia

aranceles

TTL TVC 2022

obligaciones fiscales

exenciones

Comisión Europea

ventas a distancia B2C

intelligent systems

factura electrónica

tribunales

no deal brexit

actualidad

industrial revolution 4.0

European Commission

multinacionales

european union

OMC

automatización

directiva

facturación

special taxes

Spain

fraude fiscal

Plan de Acción de IVA

mayority voting

mercados financieros

United Kingdom

TTL

special tax non reusable plastic packings

ESI

ECOFIN

taxes

indirect taxes

European Union

ecommerce

Unión Europea

impuestos

declaración de bienes en el extranjero

VAT in the Digital Age

Ley de Presupuestos

BEEPS

Italia

Digital Reporting Requirements

IVA

environmental taxation

reglas de IVA

régimen fiscal

e-iinvoicing solutions

brexit no deal

taxation

Brexit

yate

TOMS

China

Continuos Transaction Controls

DRR

alquiler vacacional

asesoramiento

impuestos especiales

economía colaborativa

MIFID II

b2c distant sales

More information

Follow us

To ensure a more efficient service provision we have developed our own collaborative online work tool, PlatformVAT.

Comments